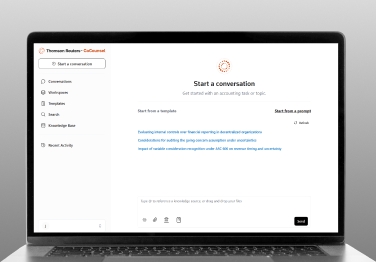

Trusted AI built on 175 years of Thomson Reuters knowledge. Meet The CoCo

TAX, AUDIT AND ACCOUNTING SOLUTIONS

Powerful AI tools and best-in-class content for tax, audit and accounting professionals

Increase efficiency, mitigate risk, and provide premium client services with enhanced AI capabilities and expert insights

Harness the power of our tax and accounting solutions

Quickly and easily find answers to even the most difficult and unpredictable tax and accounting issues with advanced search engines. Access state and global charts to cross-reference compliance regulations. Perform audits and prepare tax assessments with easy-to-use platforms that help you fact check and verify your work.

Gain access to up-to-date information on global and domestic tax issues. Find expert insights into tough accounting questions, get answers to complex scenarios, and ensure you always have the most recent compliance updates.

Our content is written by highly qualified editors who have practiced in the world's leading accounting firms, government agencies, and corporate tax departments. These subject-matter experts provide insight into complete cases and break down tough issues into digestible information.

Explore Thomson Reuters tax software for professionals

ACCOUNTANTS AND TAX PREPARERS

Tax software for accountants and tax practitioners

Increase productivity by streamlining and automating tax workflow with authoritative research tools and real-time updates to tax code changes

Corporate Professionals

Business tax software for medium and large organizations

Ensure accuracy across thousands of transactions with scalable tax products built specifically for the unique challenges of large, multi-entity corporate environments

See firsthand how our products can help

Time-consuming returns and audits are a thing of the past. Optimize efficiency with premium solutions from your trusted global technology and innovation partner.

AI that’s purpose-built for your firm, your people, and your pressure points

CoCounsel understands that tax and audit professionals' demands don’t stop at deadlines. From research to document review, it combines generative and agentic AI with task automation to help your team move faster, stay sharp, and focus on what matters most.

Unlock several advanced solutions with this single suite of products

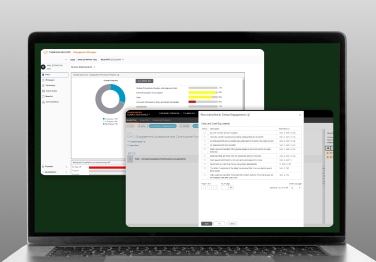

Complete audits faster with a comprehensive solution that leverages the gold standard in audit methodology and latest AI technology. Cloud Audit Suite is the ideal solution to manage audits, reviews, compilations, and preparations in one place.

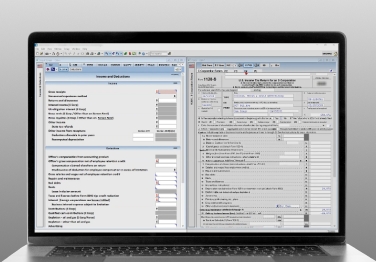

Tax returns take time, but we can help you cut that time

Professional tax software for tax preparers and accountants, including a full line of federal, state, and local programs. Save time with tax planning, preparation, and compliance.

Take a look at what other tax professionals are saying

Checkpoint Edge

"There’s obviously been a lot of thought put into the Checkpoint Edge platform itself; it is easier to drill down into, it’s more user friendly."

T.C. Burgin

CPA

Cloud Audit Suite

“The methodology and risk assessment from the audit standpoint was the other big driver that aligned with what we needed as a firm.”

Stephen Noon,

Managing Partner, Mercadien

Questions about our products and services? We’re here to support you.

Contact our team to learn more about our tax, audit, and accounting solutions.