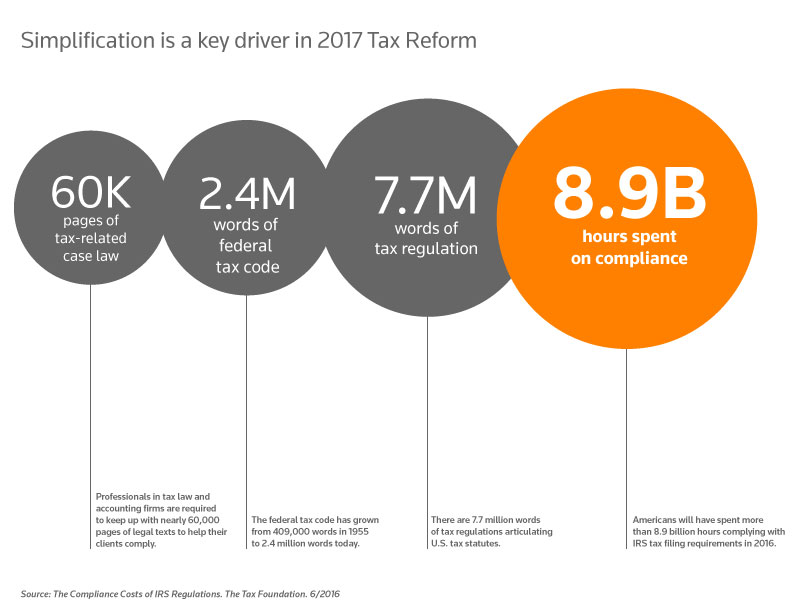

Tax reform has been a hot topic and a high priority for the Trump administration and Congressional leadership. Back in April, the administration released a one-pager outlining its priorities for reforming individual and business taxes to help grow the economy, simplify tax rules, provide relief to middle-income families, and enhance global competiveness. Although the “proposal” was short on details, it offered insights into the direction that tax reform may be headed. The administration indicated it would hold listening sessions with stakeholders during May and continue working with Congress to craft a bill that would achieve its goals.

Where are we now?

Subsequently, in late July, House Speaker Ryan, Senate Majority Leader McConnell, Treasury Secretary Mnuchin, National Economic Council Director Cohn, Senate Finance Committee Chair Hatch, and House Ways and Means Committee Chair Brady issued a joint statement on tax reform. These leaders, who have been popularly referred to recently as the “Big Six” of tax reform, indicated that the White House and Treasury have met with over 200 members of Congress and hundreds of grassroots and business groups to talk and listen to ideas about tax reform. From these meetings and many years of Congressional examination of tax reform options, the Big Six have outlined their mission as follows:

- Protecting American jobs.

- Making taxes simpler, fairer, and lower for American families.

- Lowering rates for small businesses so they can compete with larger ones.

- Lowering rates for all American businesses so they can compete with foreign ones.

Flowing from their mission, the Big Six’s goal is a plan that—

- Reduces tax rates as much as possible,

- Allows unprecedented capital expensing,

- Places a priority on permanence, and

- Creates a system that encourages American companies to bring back jobs and profits trapped overseas.

The Big Six expressed confidence that, without transitioning to a new domestic consumption-based tax system, there is a viable approach for ensuring a level playing field between American and foreign companies and workers, while protecting American jobs and the U.S. tax base. Thus, they have agreed to abandon the border adjustment tax (BAT) that was a component of previous Congressional proposals.

What’s up next? According to the Big Six, tax reform legislation is expected to move through Congressional committees this fall, with subsequent consideration on the House and Senate floors. They indicated that the President supports this approach and they invited participation by Congressional Democrats.

Subsequent to this announcement by the Big Six, White House Legislative Affairs Director Short outlined the administration’s planned schedule for passing tax reform legislation before year’s end, which he termed “aggressive.” The measure would be drafted under the reconciliation process, so that it could pass in the Senate with a simple majority. Under the plan, a 2018 budget resolution would be agreed upon in September or October; a markup and hearings on the bill would take place after Labor Day; the House would pass the bill in October; and the Senate would pass the measure in November.

So while we are waiting for specifics to emerge from Congress, we do have insight from the administration’s April one-pager, as outlined below.

Administration proposals affecting individuals

On the individual side the focus is on expanding the tax base and lowering the tax rates to support the expressed goals of tax simplification and tax relief. These would be accomplished primarily by eliminating deductions currently available and reducing the top tax rate and number of brackets.

Lower tax rates on ordinary income. The proposal calls for reducing the number of tax brackets on ordinary income from seven (ranging from 10% to 39.6%) to three tax brackets of 10%, 25% and 35%. The range of income subject to tax in each bracket was not specified.

Observation: The proposal did not indicate if the Head of Household filing status would remain (it would have been eliminated in a prior proposal).

Tax rate on capital gains and dividends. The proposal did not specify the tax rate for capital gains and dividends. In the press briefing National Economic Council Director Gary Cohn commented that it would be 20%.

Increased standard deduction. The standard deduction would be increased to $12,700 for single filers and $25,400 for married filing jointly. This would reduce the number of taxpayers who would currently itemize their deductions.

Eliminate targeted tax breaks. The proposal would eliminate “targeted tax breaks that mainly benefit the wealthiest taxpayers”. It did not provide any specifics on which breaks would survive. However, Treasury Secretary Steven Mnuchin and Cohn provided the following insights in the press briefing.

- Itemized deductions. The proposal would eliminate all itemized deductions except those for home mortgage interest and charitable contributions. Observation: There was no mention of capping total itemized deductions at $200,000 for married filing jointly and $100,000 for single filers (as in a prior proposal). Cohn indicated that the deduction for state and local income taxes would be eliminated.

- Retirement savings. Although not addressed in the proposal, Cohn indicated support for continuing deductions for retirement savings.

Repeal the alternative minimum tax (AMT). The Trump proposal would repeal the alternative minimum tax. Originally designed to ensure wealthy individuals do not avoid paying tax, it creates a dual tax system that adds significant complexity to complying with the tax rules.

Repeal the 3.8% tax on net investment income. The 3.8% tax on net investment income was enacted as part of the Affordable Care Act. It would be repealed under the Trump proposal.

Child and dependent care expenses. The proposal indicates there would be tax relief for families with child and dependent care expenses. No details were provided.

Observation: A prior Trump proposal would have provided an above-the-line deduction for children under age 13, a refundable credit of up to $1,200 a year for childcare expenses, and a savings account for child and dependent care and tuition.

Repeal the estate tax. The proposal calls for the repeal of the estate tax.

Observation: No mention is made of a prior provision that would tax unrealized appreciation on assets held at death to the extent the gains exceeded $10 million.

Administration proposals affecting businesses

The business tax proposals continue the approach of broadening the base and lowering tax rates in support of the goals to simplify the tax structure and grow the economy. They also call for a switch to a territorial tax system that would “level the playing field for American companies.”

15% tax rate on businesses. The proposal calls for lowering the corporate tax rate to 15% (the current maximum corporate rate is 35%). The 15% rate would also apply to passthrough businesses [i.e., partnerships, S corporations, and multi-owner limited liability companies (LLCs) that choose to be treated as partnerships (as most LLCs do)] and sole proprietorships (including single-owner LLCs treated as proprietorships). Currently income from these businesses is taxed to the owner at individual rates (maximum rate of 39.6%).

Eliminate tax breaks for special interests. The proposal calls for the elimination of special tax breaks. No details of specific deductions or credits targeted for elimination were provided.

Observation: Prior proposals would eliminate depreciation and allow immediate expensing of asset acquisitions. They also retained the Research and Development credit. In addition, prior proposals called for taxing income from carried interest arrangements (e.g., hedge fund manager participation) at ordinary income tax rates (as opposed to capital gain rates under current law).

Territorial tax system. One of the major shifts from prior proposals is the switch to a territorial tax system. Currently U.S. businesses are taxed on their worldwide income. Under the latest proposal, U.S. businesses would be taxed on their domestic U.S. income. Income earned abroad would be exempt.

One-time tax on repatriated earnings. The proposal calls for a one-time tax on untaxed earnings held abroad. The rate of this tax was not specified.

What’s the plan going forward?

Back in April, Secretary Mnuchin stressed that the administration will continue to work closely with Congress to refine the proposal and develop a plan that will accomplish the stated goals. He stated “We are determined to move this as fast as we can and get this done this year.” Now, following White House Legislative Affairs Director Short’s late July outline, an aggressive timeline for tax reform to proceed is as follows:

- Congressional agreement on a budget resolution in September or October.

- Markup and hearings on a tax reform bill after Labor Day.

- Passage of a tax reform bill by the House in October, and by the Senate in November.

- Enactment into law by Presidential signature in late November or early December.

A less aggressive timeline, but perhaps a more realistic one given the recent pace of action in Congress, might see tax reform enacted into law in late December, at the earliest. Stay tuned for further updates as the prospects for tax reform continue to emerge.

Stay Informed

Sign up to receive more insights and special reports on critical tax, accounting and finance topics.

Be the First to Inform Clients About Changes in Tax Legislation and Regulations

Keeping up with and communicating the latest tax and accounting regulatory changes can be challenging and time-consuming. We can help.

Learn more

Quickly Arrive at an Answer and Take Action

Checkpoint Catalyst Intuitive Search applies layers of analysis to filter, rank, and deliver the best results with unprecedented levels of accuracy.