Highlight: Not all employees must complete the 2020 Form W-4. The IRS has designed the withholding tables to work with both the 2020 Form W-4 and prior year forms.

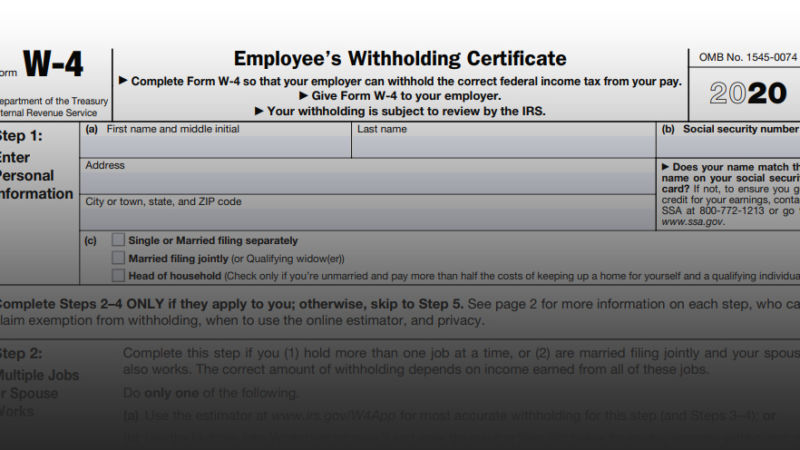

On December 5, the IRS issued the redesigned 2020 Form W-4 (Employee’s Withholding Certificate). The new form no longer uses withholding allowances. Instead, there is a five-step process and new Publication 15-T (Federal Income Tax Withholding Methods) for determining employee withholding.

The payroll community has anticipated the release of a redesigned Form W-4 since the enactment of the Tax Cuts and Jobs Act required significant changes to the form. The IRS postponed this new Form W-4 redesign in the 2018 and 2019 tax years due to time constraints and concerns from the payroll community.

Now, after two draft versions issued in June and August 2019, the IRS has issued the final 2020 Form W-4 with a five-step process (only Steps 1 and 5 must be completed) for determining employee withholding as follows:

- Step 1. For an employee’s personal information and his/her anticipated filing status to determine the standard deduction and tax rates used to compute withholding.

- Step 2. For an employee who has: (1) more than one job at the same time, or (2) are married filing jointly and both the employee and his/her spouse work.

- Step 3. Provides instructions for determining the amount of the child tax credit and the credit for other dependents that you may be able to claim when you file your tax return.

- Step 4. For an employee to enter: (1) other estimated income for the year (e.g., interest, dividends and retirement income), (2) deductions other than the standard deduction to reduce withholding and (3) any additional tax the employee wants withheld for each pay period.

- Step 5. The employee signature and date under penalties of perjury.

Not all employees must use the 2020 Form W-4

The IRS is not requiring all employees to complete a 2020 Form W-4. The IRS designed the federal withholding tables so that they will work with both the 2020 Form W-4 and prior year versions of the form. However, the following employees must use the 2020 Form W-4: (1) those hired in 2020 and (2) any employee who makes withholding changes in 2020.

Exemption from withholding

An employee may claim exemption from withholding in tax year 2020 if: (1) the employee had no federal income tax liability in 2019 and (2) the employee expects to have no federal income tax liability in 2020.

Worksheets

The 2020 Form W-4 also contains a multiple jobs worksheet to help an employee complete Step 2. An employee may instead use the IRS Withholding Estimator. If there are only two jobs total, an employee may check the box in Step 2(c). The other worksheet is for help with claiming deductions other than the standard deduction in Step 4(b).

Nonresident alien (NRA)

The 2020 Form W-4 instructions advise a NRA to view Notice 1392 (Supplemental Form W-4 Instructions for Nonresident Aliens) before completing the 2020 Form W-4. There will also be instructions in the 2020 Publication 15-T on the additional amounts that should be added to wages for determining NRA withholding.

Final version changes

Previously, the IRS explained that the second draft version and the final version of the 2020 Form W-4 would be very similar. As such, there are not many differences to note between the second draft and final version other than some wording and other small changes.

For example, in Step 2, the “Caution” note was changed to a “Tip” explaining that to be accurate submit a 2020 Form W-4 for all other jobs and use the withholding estimator if there is self-employment income. Also, the multiple jobs worksheet is more specific to say it is for Step 2(b). In addition, the higher and lower paying job wage and salary tables for employees with multiple jobs on page five now have the dollar amounts filled in.

IRS FAQs on the 2020 Form W-4

Back in August 2019, the IRS posted a list of frequently asked questions (FAQs) on the draft 2020 Form W-4 for both employers and employees. FAQ number 15 for employers explains that it may not be necessary for an employer’s software to have two different payroll systems – one for forms submitted prior to 2020 and one for forms submitted after 2019 – since the same set of withholding tables will be used for both sets of forms.

Publication 15-T

The IRS expects to release Publication 15-T in December 2019, which will be used by employers and payroll providers to calculate federal income tax withholding with the new 2020 Form W-4. The IRS already made an early release of the percentage method tables for automated payroll systems that will be included in Publication 15-T on November 26.