Sales tax and use tax are important sources of revenue for the government but properly calculating, collecting, and reporting these taxes can quickly get complicated. This is especially true as companies grow and increasingly reach consumers outside of their geographic borders.

People are probably most familiar with sales tax but an important indirect tax that is not to be overlooked is use tax. In fact, each state that imposes sales tax levies a use tax for purchases made outside of the state.

The reality is that the taxing authorities want consumers to pay a tax on all purchases they make. Therefore, businesses must understand both sales and use tax, know the differences and similarities, and have the resources to help them ensure compliance.

Jump to ↓

| What is use tax? |

| What is nexus? |

| Sales tax vs. use tax |

| Summary |

What is use tax?

Use tax is a tax that is imposed on the use, storage, or consumption of goods and services that were purchased without paying sales tax. It is typically imposed by the state or local government where the goods or services are used, and the rate is often the same as the sales tax rate. It is designed to ensure that people who purchase goods and services from out-of-state vendors or online retailers pay the same amount of tax as they would if they purchased the goods or services locally. Like sales tax, use tax revenue is used to fund various government programs and services.

While both sales and use tax are paid to the government on the purchases of goods or services, there are notable differences in how they are collected and paid to the government.

Each state that imposes sales tax levies a use tax for purchases made outside of the state. This is so state residents cannot avoid sales tax by buying taxable goods via the Internet, or even through a catalog, or the phone.

How does use tax work?

Use tax most often occurs when a consumer orders goods from outside of the state (such as online) and the retailer (not having nexus, or presence, in the consumer’s state) does not have to charge sales tax on the purchase. When this happens, the burden of remitting the tax to taxing authorities shifts to the consumer.

To further explain, let’s take a look at how two different states — in this case, Washington and Massachusetts — approach use tax.

In Washington state, use tax, which applies to both businesses and individuals, applies to items being used in the state where sales tax has not been paid. Each new owner of an item is charged with paying the use tax.

The use tax rate is the same as the sales tax rate where the item is being used and is due when the item is first used in the state. It is calculated on the value of the property, which is typically the purchase price. Every calendar year due date, the taxpayer can pay when filing their income tax.

In Washington state, in-state use tax dues occurs when the following:

- Items are purchased over the Internet (or via the phone or catalogs), without paying sales tax, and are delivered to Washington for use in the state.

- A consumer item is purchased in another state, without paying sales tax, is brought into Washington for use.

- Items purchased in Washington where sales tax has not been paid. This includes items purchased through private parties.

When purchasing vehicles, use tax usually is paid to the Department of Licensing at the time of registration. For other items, however, Washington state requires that use tax be reported on a designated tax return. For instance:

- If it is a registered business, they must report use tax on their regular excise tax return.

- If it is an individual or a business not required to register with the Department of Revenue, use tax gets reported on the Consumer Use Tax Return.

In Massachusetts, use tax must be paid on tangible personal property (including items ordered online, via the phone, or through mail order, as well as electronically transferred software) or certain telecommunications services in which the following apply:

- No sales tax (or a sales tax rate less than the 6.25 percent Massachusetts rate) was paid, and

- It is to be used, stored, or consumed in Massachusetts.

Examples of use tax

To further illustrate how use tax works, let’s explore a few examples of use tax.

As noted earlier, Massachusetts requires that use tax be paid on tangible personal property or certain telecommunications services if certain conditions apply. So let’s assume that you purchased some furniture for your Massachusetts business or home.

According to the state, if you buy furniture for your Massachusetts business or home from an out-of-state company, you don’t pay sales tax, but you still have to pay the use tax. The use tax applies because the furniture wasn’t subject to a sales tax in the other state and because it’s for use in Massachusetts. The buyer generally pays the use tax directly to Massachusetts.

Another example is California. For businesses, purchases of equipment, supplies, and books would be subject to tax. Purchases not subject to tax include food for human consumption, and electronically downloaded software, music, and games (if no tangible storage media is obtained).

So, let’s say a company purchased a case of printer paper online for use in its business. The case of printer paper cost $75, including shipping. They had it sent to their office and were not charged tax during the purchase. How much use tax does the business owe?

Answer: First, find the business’s local tax rate. Let’s assume the local rate is 8.0%. The business would then owe $6 in use tax ($75 x .08 = $6), in this scenario outlined by the state government.

(Note: Shipping charges are generally not taxable when items are shipped by common carrier or U.S. Mail, the invoice separately states charges for shipping, and the charge is not higher than the actual cost for shipping.)

As it relates to personal use, California states that, generally, an item is subject to use tax if it would have been taxable if purchased from a California retailer. This includes items like clothing, appliances, toys, books, and furniture.

What is nexus?

If you look up the word “nexus” in the dictionary you’ll see it is defined as a connection or link. Furthermore, the word comes from nectere, a Latin verb meaning “to bind.” Nexus refers to the connection between a business and a state or jurisdiction. In the context of use tax, nexus is important because it can determine whether a business is required to pay use tax on items that were purchased outside of the state but are used within the state. Therefore, it makes sense that, when it comes to sales and use tax, nexus is the tie between a seller and a state that requires the seller to collect and remit sales tax to the state.

If a business has nexus in a state, they are typically required to pay use tax on items that they bring into the state for their own use, even if those items were not subject to sales tax when they were purchased. The specific rules for when use tax applies can vary depending on the state and the circumstances of the transaction, but generally speaking, businesses with nexus in a state are more likely to be subject to use tax than those without nexus.

Economic nexus and physical presence are the most common forms of nexus.

Economic nexus

Sales tax nexus, which is more commonly referred to as economic nexus, is created when an economic activity occurs. Economic nexus refers to the type of nexus that is established based on a business’s economic activity within a state, rather than its physical presence. This means that even if a business does not have a physical location or employees in a state, they may still be required to collect and remit sales tax if they meet certain economic thresholds. These thresholds are typically based on the number of sales or transactions that a business has within the state over a certain period of time. Economic nexus has become increasingly common in recent years, as more states have adopted laws requiring out-of-state businesses to collect and remit sales tax based on their economic activity within the state.

So, states usually have economic nexus thresholds in place and businesses may be required to register in that state and collect sales tax if they exceed the economic nexus threshold. This is regardless of where the business, warehouses, or employees are located.

The South Dakota v. Wayfair Supreme Court ruling marked a major shift in tax law precedent and established a new definition of nexus.

Before Wayfair, nexus depended on a company’s “physical presence” in the state. However, as a result of the rulings, if a business sells goods in any state — even if they do not have a physical presence in that state and the transaction is online only — it may now be obligated to register in that state and collect sales tax.

This means that, with nexus decided by different thresholds in different jurisdictions, businesses must follow nexus laws across all 50 states, rather than only those in which they have physical operations.

In today’s tech-driven market, it is critical that companies that do business digitally have the proper tools and solutions in place to ensure compliance with use tax requirements.

Physical presence nexus

Physical presence nexus refers to the type of nexus that is established when a business has a physical presence in a state. This could be because they have a physical location in the state, such as an office or warehouse, or because they have employees or make a certain amount of sales within the state. In the context of sales tax and use tax, physical presence nexus is one of the most common ways that a business can be subject to tax laws in a particular state. However, it’s important to note that not all states require physical presence to establish nexus, and there are other types of nexus that can also apply.

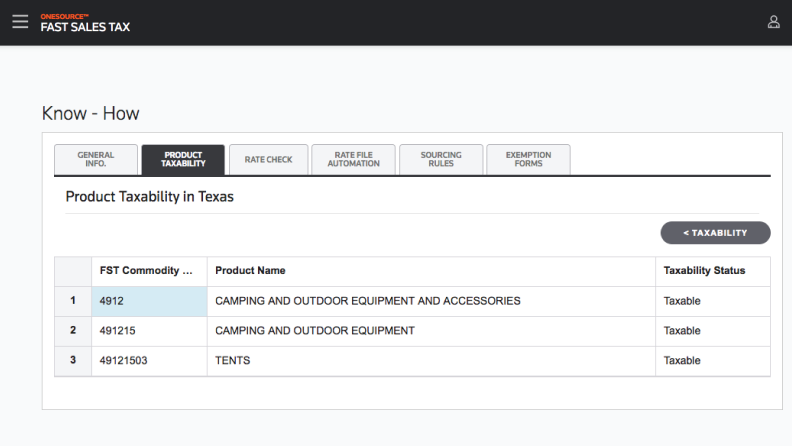

ONESOURCE Fast Sales Tax

Real-time tax rates, due dates, and taxability statuses to stay compliant

Learn more ↗Sales tax vs. use tax

The main difference between sales tax and use tax is in the point of collection. Sales tax is collected by the seller at the time of the sale, while use tax is paid by the buyer when they use or consume a product or service purchased from an out-of-state vendor. Sales tax is typically imposed on all sales made within a jurisdiction, while use tax is only imposed on purchases made from out-of-state vendors. Use tax can be intended to ensure that all purchases are subject to taxation regardless of whether they were made in-state or out-of-state. Both sales tax and use tax are important sources of revenue for state and local governments and are used to fund public services and infrastructure projects.

It can be easy to confuse sales tax and use tax as there are some similarities; however, there are some notable differences. Therefore, it is important to understand the distinction between the two.

To briefly recap, sales tax and use tax are both a form of indirect tax, which means they are a tax that can be shifted to others. And while sales tax and use tax are both remitted to the government, there are differences in how they are collected and paid to the government.

Sales tax is collected by a company on the retail sales of goods and services when the final sale in the supply chain is reached. It is added to the sales price of goods and services and then charged by the retailer to the end consumer. The retailer is responsible for remitting that collected tax to the government.

Use tax, on the other hand, refers to the tax imposed on the taxable goods and services that were not taxed at the point of sale. Unlike sales tax, the consumer is typically responsible for remitting use tax.

Also, there is is exemptions to some taxable items. Items exempt from sales tax are also exempt from use tax as well.

Understanding use tax can be confusing and many businesses are not too familiar with the finer details. They may have even made purchases that are subject to use tax and are not even aware. That’s why leveraging the right tools and solutions to ensure compliance is critical.

Summary

In conclusion, use tax is a type of tax that is imposed on goods or services that are purchased from out-of-state vendors and used or consumed within a state. It is a complementary tax to sales tax and is intended to ensure that all purchases are subject to taxation regardless of whether they were made in-state or out-of-state.

Use tax can be a complex and confusing topic, but it is important for businesses and individuals to understand their obligations and comply with the law to avoid potential penalties and fines. By staying informed and working with trusted advisors, businesses and individuals can navigate the complexities of use tax and ensure that they remain in compliance with state and local tax laws.